Farm Loans for Beginning Farmers in Australia

You have found the country, run the numbers, and the cattle are out there waiting. The thing standing between you and your first herd is usually finance.

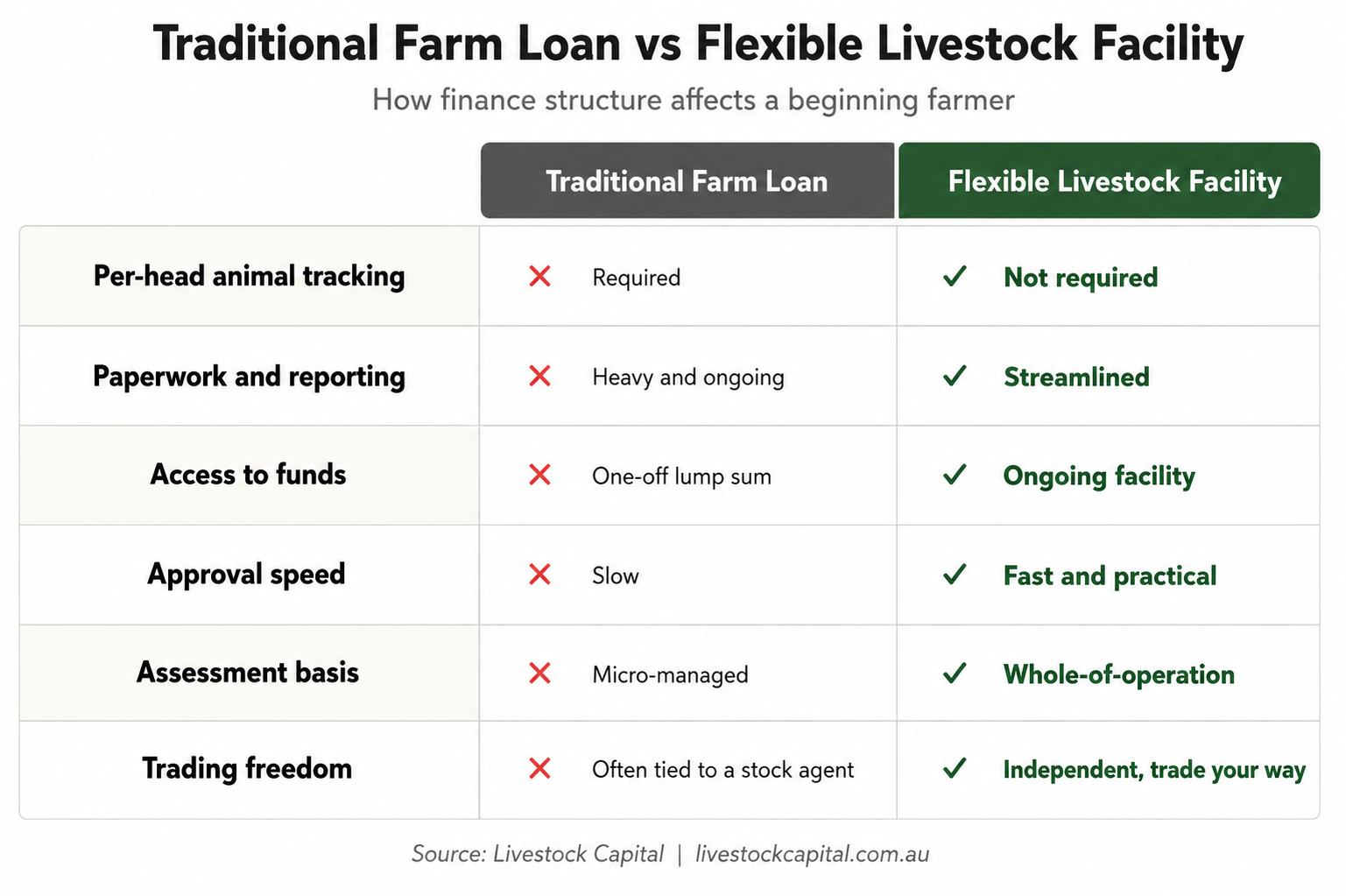

For many new producers the bottleneck is not skill or confidence. It is the slow approvals, heavy paperwork and rigid conditions that come with traditional agricultural lending. Farm loans for beginning farmers in Australia have a reputation for being hard work, and that reputation is mostly earned.

Old lending models were built around established operators with years of records and plenty of equity. When you are just starting out, that model can feel like it was designed to keep you out.

The good news is that funding your first herd does not have to mean overextending or signing up for years of restrictive monitoring. This guide explains how flexible livestock finance works, what to watch for, and how to grow a herd at a pace your cash flow can handle.

Why Farm Loans for Beginning Farmers Feel Harder Than They Should

Buying cattle is capital intensive. A modest starting herd can tie up six figures before you have sold a single beast, and that is before fencing, water, feed and freight.

Most new producers do not have that cash sitting idle, so finance becomes the bridge between the opportunity in front of you and the working capital you actually hold. The trouble is that traditional livestock finance was not built with new entrants in mind.

The Paperwork and Tracking Burden

Many conventional lenders want detailed, ongoing reporting. Some require per-head tracking, where individual animals are monitored as security. That means tagging, counting and reconciling stock for the bank rather than for your operation. For a beginning farmer still finding their feet, that is hours of admin pulling you away from the paddock.

Slow Approvals and Missed Cattle

Cattle markets move fast. A line of good steers at the right weight and price can appear and sell within a week. Traditional approvals rarely move at that speed, so the opportunity often goes to a buyer who already had funds ready.

The Hidden Cost of Rigid Finance

Restrictive finance carries costs that never show on a rate sheet. Capital sits locked up, decisions get delayed, and growth is rationed to what the lender is comfortable with rather than what your operation can support. For new entrants, access to finance ranks among the biggest barriers to getting started, alongside land prices.

What Beginning Farmers Actually Need From Livestock Finance

Set finance features aside for a moment and think about outcomes. When you are building a herd from scratch, you need finance that does a few simple things well:

- Working capital to buy stock without draining every dollar you hold.

- Fast decisions so you can act when the right cattle come up.

- Flexibility to buy in stages as your cash flow grows.

- Light-touch reporting that respects your time.

- Clear terms you can understand without a finance degree.

Cash Flow That Matches the Cattle Cycle

Cattle do not earn income the day you buy them. There is a gap between purchase and sale, and that gap is where many new operations get caught short. Good livestock finance is built around that reality, freeing up working capital so you are not forced to sell early just to cover the next bill.

Room to Grow at Your Own Pace

You do not have to build the whole herd in one go. A facility you can draw on as needed lets you start smaller, prove the model on your own country, then scale.

This staged approach is one of the most practical ways to fund your first herd without overextending, because you match borrowing to genuine opportunity rather than borrowing big and hoping. Livestock loans in Australia work best when they bend to your operation, not the other way around.

Livestock Finance Options and How to Choose

Not all farmers loans are the same. Understanding the main structures helps you pick what suits your operation and your stage.

Term Loans vs Flexible Facilities

A term loan gives you a lump sum repaid over a set period. It suits a single, defined purchase such as a foundation herd. A flexible facility works more like an approved limit you draw against as needed, which suits producers who buy and sell through the year and want ongoing access rather than reapplying each time.

Secured vs Unsecured, Loans vs Lease

Secured finance is backed by an asset, often the livestock or land, and usually carries lower rates. Unsecured finance needs less collateral but tends to cost more, so for most new producers secured livestock finance offers the best balance.

Funding can also be structured as a loan or a lease, which can help with cash flow and tax planning. Livestock Capital arranges either, with limits from $100,000 to $6 million subject to approval, so the structure is matched to the operation rather than forced into one mould.

Government-Backed Options

Concessional options exist too. The Regional Investment Corporation’s AgriStarter Loan is designed for first farmers and offers long, low-cost terms, though eligibility can be strict and timelines longer. It is worth knowing about as part of the bigger picture rather than the whole answer.

The Cost of the Wrong Finance Structure

Choosing the wrong finance is not just an inconvenience. It can quietly cap how fast, and how safely, your operation grows.

Missed Cattle and Forced Sales

The clearest cost is the cattle you never buy. When funds are slow or locked up, well-priced stock passes you by, and over a few seasons those missed lines add up to real lost income. Rigid repayments that ignore the cattle cycle can also force you to sell at the wrong time, eroding hard-won margin.

Admin That Pulls You Off the Farm

Every hour spent reconciling per-head reports for a lender is an hour not spent on stock, pasture or planning. For a small, growing operation that time is one of your scarcest resources.

Borrowing in the Wrong Shape

There is also the risk of borrowing too much, too rigidly. About half of Australian broadacre farms carry some debt, and the Department of Agriculture, Fisheries and Forestry’s ABARES tracks how that debt sits across the sector.

Healthy debt funds productive assets that earn more than they cost. The danger is a structure that will not flex when seasons or markets turn. The aim is not to avoid finance, but to use the right structure so it works for the farm rather than against it.

How to Fund Your First Herd Without Overextending

A sensible approach to finance is the difference between steady growth and a stalled start. A few principles go a long way.

Start With Your Needs, Not the Maximum Loan

Work out what your operation genuinely needs to run and grow over the next twelve months, then borrow against real needs and real opportunities rather than the biggest number a lender will offer.

Build to the Market

The market backdrop matters. Meat & Livestock Australia projects the national herd to stay above 30 million head in 2026, with cattle slaughter at its highest level in almost five decades. Supply and demand shape what cattle cost and return, so plan your herd around where the market is heading, not only where it sits today.

Keep Some Headroom

Leave room to move. A facility you can draw on when an opportunity appears is worth more than a fully drawn loan with nothing left. Headroom is what lets you act fast without overextending.

Watch for the Warning Signs of the Wrong Provider

A few signals that it may be time to look elsewhere:

- You spend more time reporting to the lender than running the farm

- Approvals are too slow to act on real cattle opportunities

- You feel locked into a particular stock agent or selling channel

- Terms are unclear, or conditions appear that you did not expect

How Livestock Capital Works

Livestock Capital is built around a simple idea: finance should support farm growth, not add to the workload. It works with beef, dairy and sheep producers across Australia.

Operation-Based Assessment

Rather than monitoring individual animals, the focus is on how your operation performs as a whole. That means no per-head tracking and far less of the reporting that bogs down traditional agricultural finance.

Fast Approvals and Flexible Facilities

Decisions are made efficiently so you can act on opportunities while they are still in front of you. The process is straightforward: assessment, approval, then access to your facility. Funding comes as loans or lease arrangements with competitive, risk-adjusted pricing, and terms are clear and upfront with no surprise conditions.

Independent, So You Trade Your Way

This is a key difference. Many livestock funders are tied to stock agents and expect you to buy and sell through them. Livestock Capital is an independent provider, so you keep the freedom to trade with whoever you choose. Your finance does not dictate your selling channel.

The same approach runs across related needs. Producers can look at cow finance and beef finance for stock, farm land finance for country, and equipment finance for the gear that keeps the operation moving.

Frequently Asked Questions

How Are Farm Loans for Beginning Farmers in Australia Different From a Regular Bank Loan?

Both provide funds, but the structure differs. Traditional bank loans often demand long records, strong equity and ongoing reporting. Flexible livestock finance focuses on how your operation performs overall, with lighter paperwork and ongoing access. That suits producers still building a track record who need to move quickly on cattle.

How Much Can I Borrow to Fund My First Herd?

It depends on your operation, your security and the opportunity in front of you. Livestock Capital offers funding from $100,000 to $6 million, subject to approval, as loans or lease arrangements. The right amount is rarely the maximum on offer. A good provider matches borrowing to genuine working capital needs.

Will I Have to Provide Per-Head Reporting on My Cattle?

Not with every provider. Traditional livestock finance often requires individual animal tracking as part of the security, which is time consuming. Livestock Capital uses operation-based assessment instead, so there is no per-head tracking. The focus stays on overall farm performance, freeing your time for the work that grows the business.

How Fast Is Approval?

Usually faster than traditional agricultural lending. The process is streamlined into assessment, approval and facility access, with paperwork kept to what is genuinely needed. Speed matters because cattle opportunities do not wait, and moving quickly can be the difference between securing a good line of stock and missing it.

Will I Be Locked Into Using a Particular Stock Agent?

No, and this is a key point of difference. Many livestock funds are connected to stock agents and expect you to trade through them. Livestock Capital is an independent provider, so you keep full freedom to buy and sell with whoever you choose. Your finance supports your decisions rather than dictating them.

Is Livestock Finance Only for Beef Cattle?

No. Finance solutions cover beef, dairy and sheep operations. Whether you are expanding a breeding herd, lifting dairy herd quality or running trading cattle, the facility is structured around how your operation works. Beef producers, dairy farmers and feedlot operators each have different cash flow patterns, and the structure suits those rhythms.

What Does Livestock Finance Cost?

Pricing is competitive and risk-adjusted, so it is tailored to each farm rather than a flat rate. The real comparison is not the headline rate alone: rigid finance carries hidden costs in missed cattle and admin time, while a flexible facility shows its value in the stock you can buy. The guide on farm loan interest rates explains what shapes your rate.

Can I Finance Land and Equipment Too, Not Just Stock?

Yes. Building an operation usually takes more than cattle. Alongside livestock funding you can finance farm land and the equipment that keeps things running, which helps protect your working capital. The guide on farm equipment finance types is a useful starting point if gear is on your list.

Farm Loans for Beginning Farmers in Australia: The Practical Way Forward

Building your first herd is a big step, and the finance behind it should make that step easier, not harder. Farm loans for beginning farmers in Australia do not have to mean slow approvals, endless paperwork or being told how to trade.

Flexible livestock finance lets you fund your first herd, protect your cash flow and grow at a sensible pace. With operation-based assessment, fast decisions and the independence to trade your way, the finance works for the farm, not against it.

If you are ready to talk through funding your first herd, Livestock Capital can help. Call

1300 980 548

to discuss a facility built around your operation and start growing on your terms.