Farm Loan Interest Rates: What Affects Your Loan Rate

When you are weighing up a herd expansion or jumping on a cattle opportunity, the farm loan interest rates on offer can be the difference between a profitable move and a stretched budget. A rate that looks small on paper adds up fast across a six or seven figure facility. For Australian producers managing seasonal cash flow, even half a percent matters.

The good news is that your rate is not fixed by luck. Lenders weigh up a handful of factors when they price a livestock loan, and several of them are within your control.

This article breaks down what actually sets your rate, how lenders read your operation, and the practical steps you can take to secure better livestock finance. You will finish knowing exactly what to ask for and what to fix before you apply.

Why Your Rate Matters More Than You Think

Most producers focus on whether they can get finance approved. Fewer stop to work out what the rate is really costing them over the life of the facility.

Consider a $1 million livestock facility. A one percent difference in your rate is roughly $10,000 a year in extra interest. Over five years, that is $50,000 that could have gone into more stock, better pasture, or a new set of yards.

That gap bites harder when seasons turn. Production costs remain a major squeeze on margins, with the Reserve Bank of Australia cash rate, exchange rate swings and input cost shocks all weighing on cattle operations. When your rate is higher than it needs to be, you have less room to absorb a dry spell or a price dip.

There is also an opportunity cost. Cattle markets move quickly. When prices are right for restocking or trading, producers locked into expensive, rigid finance often cannot act in time. By the time a slow approval comes through, the opportunity has passed.

Using the wrong finance approach makes this worse. A short-term, high-rate facility used for a long-term purchase ties up cash you need day to day. A loan buried in reporting conditions drowns you in admin instead of letting you farm.

The cost of a poorly priced loan is rarely one big hit. It is a slow drain on cash flow, flexibility and growth capacity that many producers only notice years later.

What Actually Sets Your Farm Loan Interest Rate

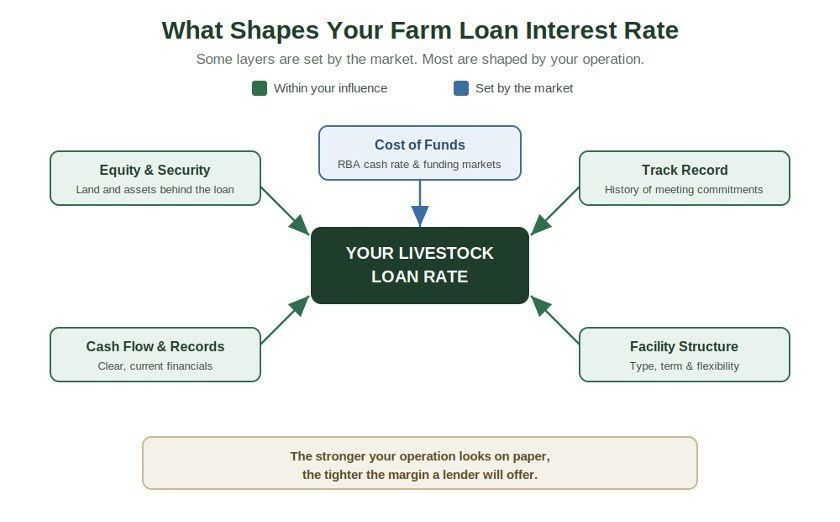

Your rate is built from several layers. Understanding each one shows you where you have leverage, and the diagram below maps how they fit together.

The starting point is the cost of funds. Lenders source money from wider markets, and the cash rate set by the Reserve Bank of Australia is the benchmark that flows through to all lending. When that benchmark moves, farm loan interest rates tend to follow. You cannot control this layer, but you can understand it.

On top of that sits your risk margin. This is the part lenders adjust based on your operation, and it is where most of your influence lies. The stronger and more secure your business looks, the tighter that margin.

Then comes the security you offer. Finance backed by land or strong assets is usually priced more sharply than unsecured lending, because the lender carries less risk.

Finally, the structure and term shape the rate. A flexible working capital line, a term loan and an equipment facility are priced differently because each carries a different risk profile. If you are new to rural lending, our overview of agricultural finance is a useful starting point.

How Lenders Read Your Operation

When a lender prices your livestock loan, they are really asking one question: how confident are we that this operation can service the debt through good seasons and bad? Three things drive that confidence.

Your equity and security come first. A higher equity position, or quality land behind the loan, lowers the lender's risk and usually your rate. Producers pairing farm land finance with livestock funding often present a stronger overall position.

Your cash flow and financial records come next. Clean, current figures that show consistent income and sensible costs make you easy to assess. Messy or incomplete records force lenders to price in uncertainty, and that uncertainty costs you.

Your track record matters too. A history of meeting commitments and managing through dry spells all counts in your favour. The Australian farm sector is, on the whole, a dependable borrower: foreclosures account for well under one percent of farm loans on issue, which is part of why lenders compete for solid agricultural business.

The clearer and stronger your operation looks on paper, the better the rate you can negotiate.

Practical Ways to Improve Your Livestock Loan Rate

You have more influence over your rate than you might think. Here is where to focus before you apply.

Tidy up your financials. Pull together current profit and loss figures, a balance sheet and recent tax returns. Lenders reward producers who can show their numbers clearly and quickly.

Strengthen your equity. Paying down existing debt or demonstrating asset growth improves how lenders see your risk. Even modest progress can shift your margin.

Match the facility to the purpose. Use working capital lines for stock and short-term needs, and term finance for land or infrastructure. Producers combining equipment finance with livestock funding can keep each facility priced appropriately.

Look past the headline rate. Compare fees, flexibility, reporting requirements and how quickly you can access funds. A slightly higher rate with no per-head tracking and fast approval can be cheaper in real terms than a low rate buried in admin.

Build a relationship with a lender who understands cattle. A specialist who reads your operation, rather than running it through a generic farmers loans template, will price you more accurately.

Structuring Finance Around Your Cash Flow

A good rate means little if the repayment structure fights your cash flow. Cattle income arrives in lumps, not even monthly instalments, so look for facilities that allow flexible or seasonal repayments aligned to your selling pattern.

For a beef producer chasing trading opportunities, an ongoing working capital line beats a one-off loan. You draw funds when the right cattle appear and repay when you sell, without reapplying each time.

For a dairy farmer with steadier monthly income, a structure aligned to that predictable cycle often works better, freeing capital for herd improvement and quality breeding stock.

For a feedlot operator, facility capacity and quick turnaround matter most. Our guide on working capital versus infrastructure finance explains how to split these needs so the structure supports high volume and fast turnover.

The right structure protects your working capital, so you can expand herd numbers without tying up every dollar. That flexibility is often worth more than a marginally lower rate.

Signs It Is Time to Review Your Finance

Some operations are quietly paying too much, or working around finance that no longer fits. Watch for these signs:

- You have not reviewed your rate or facility in two or more years, despite a stronger balance sheet.

- Your repayments do not line up with when cattle income actually arrives.

- You are spending hours on per-head reporting or paperwork your lender demands.

- You have missed cattle buying opportunities because approval took too long.

- Your equity has grown but your rate has not improved to reflect lower risk.

- You are stretching one rigid loan across several different needs.

Each of these has a cost. Delaying a review can mean thousands in unnecessary interest every year, plus the margin lost on opportunities you could not fund in time. In a competitive cattle market, producers with flexible, well-priced finance move while others are still waiting on a decision.

How Livestock Capital Approaches Your Rate

Livestock Capital was built around how cattle operations actually run, not around traditional lending templates.

We assess your operation as a whole rather than tracking individual animals. There is no per-head monitoring and no constant reporting, which strips out a layer of admin most producers dread.

Our assessment focuses on overall farm performance, your equity and your cash flow, the factors that genuinely reflect your ability to service finance. That operation-based view often lets us price and structure facilities more practically than conventional agribusiness banking.

The process is straightforward. We look at your operation, agree a facility structure that suits your cash flow, and give you ongoing access to funds rather than forcing a fresh approval every time an opportunity appears. Approval is efficient, terms are clear, and there are no surprise conditions in the fine print.

We work with cattle producers right across Australia, from single-property operations to larger agricultural business groups.

Quick Checklist Before You Borrow

Before you sign on any livestock loan, run through this list:

- Have current financials ready so lenders can assess you quickly and price you fairly.

- Check the structure, not just the rate, and make sure repayments match your cattle income pattern.

- Ask whether per-head tracking or heavy reporting applies, because that admin is a real cost.

- Test the flexibility: can you access funds again without reapplying when an opportunity appears?

- Weigh fees, approval speed and conditions alongside the headline rate.

- Review regularly, and if your equity has grown, push for a rate that reflects your lower risk.

Ask any provider these questions directly. The answers tell you far more about the true cost of your finance than the advertised rate alone.

Get Finance That Works as Hard as You Do

Your farm loan interest rates are not set in stone. By understanding what drives them, presenting a strong operation and choosing finance structured around your cash flow, you can secure a better rate and the flexibility to grow your herd on your terms.

If you are ready to expand, trade, or simply review what you are paying, Livestock Capital can help. Call

1300 980 548 to talk through your options, or apply for livestock finance today. For the bigger picture on funding your herd, explore our beef finance guide.